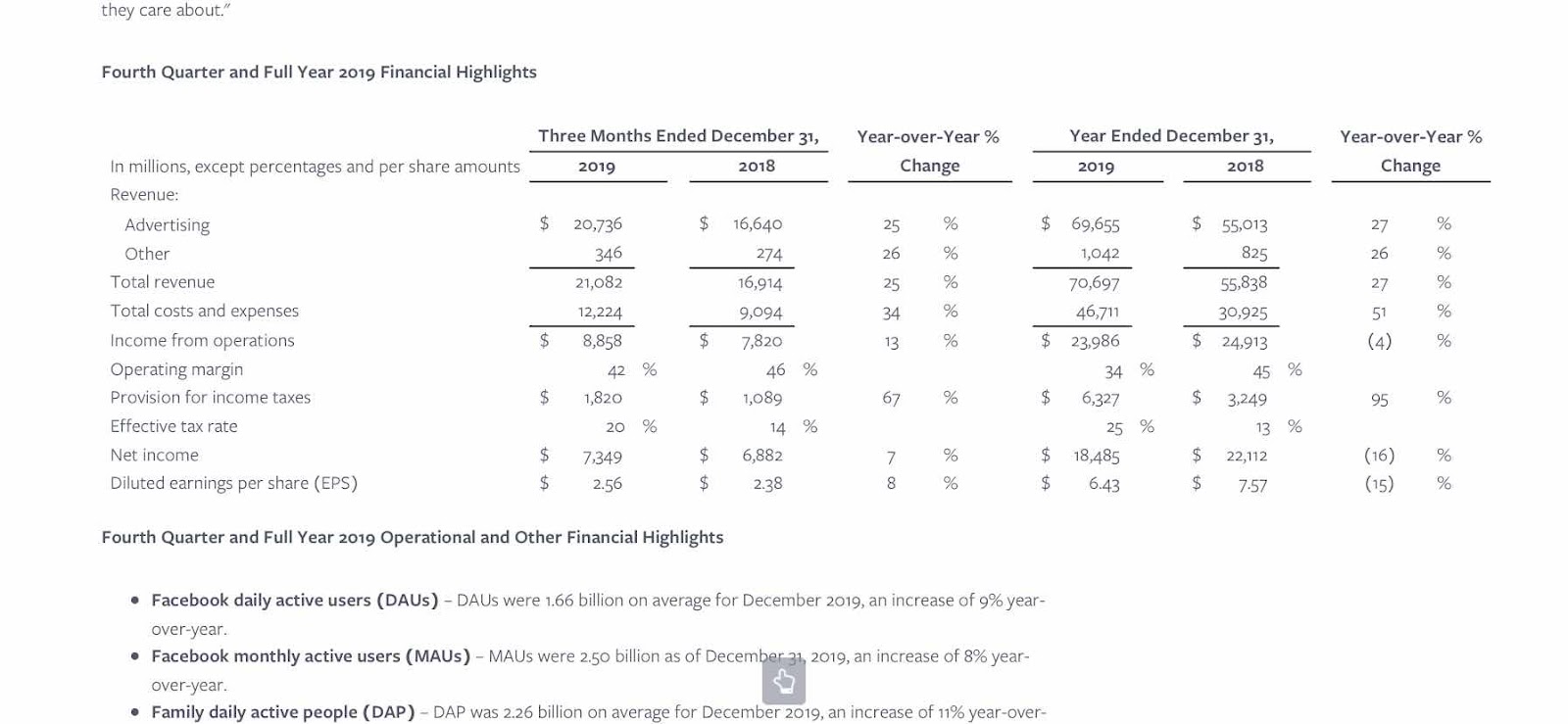

FB Reported 4Q2019 Results with revenue growing 27% year over year and expenses growing 51%. The operating profit margin for the company has reduced from 50% to 37% over the past 2 years as company has to spend more on security and data protection.

Regulation is a major concern as it will slow down the growth potential of the company. Growth has slowed from 30% to 25% and future growth over next 5 years could be 18-20% per year. This and profit taking after large run up in 2019 explains the reasons for recent correction.

This company has done an amazing job over last 5 years increasing revenue from $12.5B to $70B. Share price has also increased. Company has $57B excess cash which is $19 per share. At $202 share price today an investor is paying $183 for a business that can earn $10 Cash EPS in 2020. 18 times P/E for a business that still has monetization potential with Instagram and WhatsApp and has a dominant advertising franchise with Facebook is a very reasonable price for a long term investor. Company continues to invest in innovation in AI, Payments, VR and other avenues.

Assuming company can grow revenue at 18-20% over next 5 years and earnings 15-20% as well at a 15 P/E the stock could be valued at $300 to $350. Not as fantastic an opportunity as in Dec 2018 but in the current expensive market FB is relatively speaking a better value. Selling Jan 2022 $200 Puts for $40+ can assure a $160 effective price providing a greater margin of safety and higher return.

Major competitors are GOOGL, TWTR, SNAP, AMZN.

No comments:

Post a Comment